PDD.US

[November 17, 2018]

* Initial Analysis *

Business Model

PDD is platform-on-a-platform marketplace which leverage established social network of foundation platform to aggregate consumer demand at large volume for merchants enabling deep volume discount for consumers.

Current Monetization / Revenue Stream

Currently, PDD monetizes the marketplace by providing online marketing services to merchants and charges merchants commission fees to cover payment processing fees and other overheads. The mechanism of rake is still not built in the platform. Rake might be another revenue stream if the platform merchant profile and consumer behavior shift in the future (this might gradually happen if PDD’s attempt to build brand and trust works).

Quality Assurance Issue

PDD has been fixing counterfeit product issues. Discount-oriented marketplace is more likely to have quality assurance and trust/credibility issues to deal with.

Unit Economics & Growth Drivers

PDD monetize the marketplace directly and indirectly. Commission fee is more likely to have linear relationship with GMV while the relationship between OMS revenue and GMV is not clear at this stage. OMS revenue depends on merchant marketing spending to promote their products and how much PDD marketing service they use. Both revenue streams are driven by directly/indirectly by GMV.

GMV on the marketplace depends on how many active buyers and how much they spend on average during a given period. Average buyer spending depends on average order size and purchasing frequency in the given period.

Due to limited access to information, the modeling here starts with foundation platform MAU and applies an adoption/penetration rate to it to derive PPD MAU. Then a conversion rate is applied to PPD MAU to derive LTM active buyer. Then rolling LTM method introduces seasonality in quarterly projection. LTM GMV projection is based on active buyer and average spending assumptions.

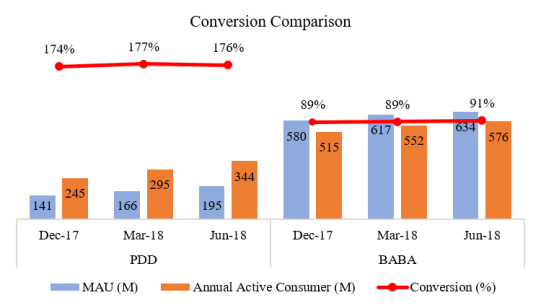

One user behavior is discovered in the conversion analysis. As PDD only discloses LTM active buyers and three month ending MAU, if the conversion rate is defined as LTM active buyer / MAU, we would find the ratio is 176%. Two implication from positive deviation from 100%: 1) Monthly period might not be an appropriate time horizon to estimate gross user base; 2) the user base might experience a high churn rate which leads to high buyer acquisition/retention/re-activation costs for the marketplace.

Compared to PDD’s number , BABA’s ~90% looks more healthy although I’m not sure whether metrics are comparable.

The aforementioned concern can be checked with unit economics analysis. It’s difficult for a marketplace suffers from high churn rate resulting from either internal/external issues to enjoy the structural cost advantage on platform. Jun-2018 LTM Contribution Profit 1 (CP1) was 12.9 RMB per active buyer while All-in CAC increased to RMB 12.9 from RMB 5.5 in Dec-2017.

Two-sided platform-on-a-platform

By leveraging the existing social network, the initial user acquisition cost for PDD is significant low compared to building up from scratch. Once the marketplace has solution demand-side in the start-up problem, it’s relatively easy to scale up the platform. PDD experienced exponential growth in the past 3 years. However, the increasing all-in CAC might indicate the network effect / scale in this type of platform business cannot protect it from competition on different value proposition.

The business model is easy for existing e-commerce players with scale to replicate. It seems switching cost at this type of marketplace is relatively, different marketplace will compete on value proposition and stickiness.

Marketing / Branding

Probably not comparable. Several years ago I had a branding lecture at HTC earnings conference call when it launched HTC Butterfly. So I didn’t feel every comfortable when I saw terms like brand awareness/recognition or concept of nurturing merchant’s own brand in the marketplace’s first earnings conference call transcript.

Cashflow

The good news is that it seems this marketplace is able to extract working capital from merchants when scaling up. Thus, if there’s no other major capital expenditure in the near future or ridiculous marketing campaign, PDD should have no additional external financing need.

Mezzanine Equity

It might be better to figure out the mechanism of the mezzanine equity base.

What to bet on?

This is a listed start-up: 1) execution on current business plan; 2) pivoting optionality; 3) acquisition target. The analysis should focus on its founder and management team.

~ Corporate Event~

- PDD to report its unaudited financial results for the third quarter ended September 30, 2018, before U.S. markets open on Tuesday, November 20, 2018.

- Earnings conference call at 8:00 AM U.S. Eastern Time on November 20, 2018 (9:00 PM Beijing/Hong Kong Time on the same day).

~ Materials ~

2 thoughts on “PDD.US – Initial Analysis”